Filing your taxes can seem daunting at first.

I mean, why is your employer sending you all these forms in the mail? What’s a W-2? A 1099? What receipts should you keep? What deadlines are approaching?

Moreover, are you going to get money from the IRS? Or are you going to owe money come April 18th?

On the surface, it’s all pretty confusing. But once you see the bigger picture — the whole A to Z process and how it works — it all starts to make way more sense.

So let’s do that now!

Here’s how to file your taxes, step-by-step.

What’s Ahead:

1. Understand taxes and how they work

Even if we determine in Step 2 that you don’t need to file taxes this year, it’s important for you to understand what they are and how they work.

Not only because you’ll almost certainly be paying taxes eventually, but because understanding our tax system is fundamental to our functioning democracy.

Generated using imgflip.com

I mean that quite literally. The whole reason the U.S. broke off with Britain is because enough citizens understood our current tax system and that it was total B.S.!

On a more fundamental level, understanding taxes will also help to ensure you file them properly moving forward. Because the Internal Revenue Service (aka IRS, the agency responsible for collecting taxes in this country) ain’t messing around.

Remember: they’re the ones who caught Al Capone when no other federal agency could. More recently, they’ve somehow managed to outsmart tax dodgers who hid their gains in crypto.

Point being, everyone should understand how taxes work.

And thankfully, they’re pretty simple.

How taxes work, in a nutshell

Taxes are basically your “subscription fee” to America. In order to use the roads, public schools, Medicare, the fire department, and other civil services, you gotta pay taxes.

Taxes also help pay for other government-funded initiatives, such as space exploration, tech and medical research, and our military.

Now, not everyone pays the same “subscription fee.” The U.S. uses a “progressive” system where you pay certain percentages for different chunks of your income.

It’s easier to explain once I share the tax rates for 2022 (the year you’ll file for in 2023):

| Tax rate | For single filers | For married individuals filing joint returns |

|---|---|---|

| 10% | <$10,275 | $20,550 |

| 12% | $10,275 - $41,775 | $20,550 - $83,550 |

| 22% | $41,775 - $89,075 | $83,550 - $178,150 |

| 24% | $89,075 - $170,050 | $178,150 - $340,100 |

| 32% | $170,050 - $215,950 | $340,100 - $431,900 |

| 35% | $215,950 - $539,900 | $431,900 - $647,850 |

| 37% | $539,900+ | $647,850+ |

Now, let’s say you’re single and made $50,000 in 2022.

- Your first $10,275 will be taxed at 10%

- All the money you made between $10,275 and $41,775 (aka $31,500) will be taxed at 12%

- All the money you made between $41,775 and $50,000 (aka $8,225) will be taxed at 22%

It’s a common misunderstanding that as soon as you make more than $89,075, all of your income will be taxed at 24%. Thankfully for anyone who got a raise last year, that’s not how it works. If you made $89,076, exactly $1 of your income would be taxed at a rate of 24%.

Now, in addition to federal income taxes, you may also have to pay state income taxes. Only nine states don’t charge state income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming.

As for folks in the other 41, some states have a flat rate (Colorado = 4.55%) while others have a progressive rate (Georgia = between 1% and 5.75%). Filing your state income taxes is usually much easier than federal, and the professional and DIY solutions we’ll discuss below will help you take care of it.

But for the purposes of the rest of this article, we’ll focus on federal taxes since that’s 90% of the work!

2. Determine if you even need to file taxes for 2022

Broadly speaking, if you made more than $12,950 in net income last year, you probably need to file your taxes. Even if you didn’t, you might still benefit from filing a tax return, anyways.

Oh, and “filing a return” is just another way of saying filing your taxes. For clarity on more tax-related lingo, jump down to our tax term glossary below.

You may not need to file a tax return if you’re:

- Under the age of 65

- Single

- Earned less than $12,950 in 2022

- Don’t have any other special circumstance or sources of income that would require you to still file (e.g., unemployment income, self-employment income, etc.)

If you meet all of those, you don’t have to file a tax return.

But you might want to, nonetheless.

Why you might still want to file a tax return (even if you don’t have to)

The IRS lists a few bonafide reasons why it’s still worth your time to file a return, even when you’re not required to. Here are the big three:

- You might still get a refund — if your employer withheld some of your paychecks for taxes and you ended up making less than $12,950, you’re actually entitled to get some or all of that money back. The same goes for if you qualified for the earned income tax credit, child tax credit, etc.

- It helps you apply for financial aid — If Uncle Sam already has an accurate picture of your income (or lack thereof) from your tax returns, it’ll make it easier and faster to approve you for aid in the future.

- You’ll earn more Social Security later — Underreporting your self-employed income can not only get you in trouble but can shrink how much you make from Social Security later, since the IRS bases that amount on how much you pay in Social Security taxes during your income-earning years.

Speaking from personal experience, it’s also just good practice. You get familiar with the forms, what goes where, and all that other jazz while everything’s way simpler and the stakes are much lower.

Now that we’ve (hopefully) determined that you’re filing either way, how much time do you have?

3. Know your deadlines

Your next step is to mark your calendars for some key dates. You’ll certainly want to have all your ducks in a row well before April 18, 2023, when your taxes for 2022 are due!

TurboTax has a super helpful list of every possible deadline between now and tax day 2023, but here are the big hitters that will most likely apply to you:

- January 23 — Tax season officially began, meaning this was the first day the IRS would accept your 2022 tax returns.

- January 31 — Due date for employers to send out W-2 and 1099 forms. Your W-2 is essentially your record of employment at a salaried job that includes how much you earned last year. It looks like this, and you’ll need it to file your taxes. A 1099 looks just like a W-2, only it’s for independent contractors, not salaried employees. Now, January 31 is just the deadline to send these forms. If you haven’t received your W-2 or 1099s by Valentine’s Day, you might want to reach out to your employer/client.

- April 18 — This is the day your tax return is due and is the closest thing we have to an anti-holiday in this country (save, perhaps, Columbus Day?). To be honest, I’m not sure why people dread tax day. I mean, most people get an average refund of $3,200, which is a helluva lot more than you get on your birthday. But I digress. You gotta get your filing done by midnight on April 18. And the consequences for missing the deadline range from none at all to pretty sticky.

What happens if I miss the deadline on my taxes?

For starters, if you know you’re going to miss tax day, you can file for an extension before April 18. If approved, the IRS will extend your deadline to October 16 and charge a nominal interest rate on your taxes owed but no penalties.

But don’t file for an extension unless you really need it.

If you straight up miss tax day, the IRS will charge you a fee of 5% of the taxes you owe each month until you pay up. If you’re self-employed and owe, for example, $15,000 in taxes, 5% ($750) can rack up quickly.

Now, if you fail to file by April 18 and the IRS owes you money (which is typically the case with W-2 employees), they won’t care as much. You’ll only get hit by a Failure to File fee, which maxes out at the lesser of $435 or 100% of your total taxes paid that year.

In other words, if the IRS owes you money and you don’t come get it, they basically go:

¯\_(ツ)_/¯

Each year, Americans leave over $1 billion in unclaimed refunds on the table with the IRS. And it’s not really the IRS’s fault for “withholding” it, since they can’t send your money without your tax return.

The IRS when Americans leave $1 billion in unclaimed refunds each year |

Generated using imgflip

All the more reason to file your taxes even if you think it’s not necessary!

4. Gather all your documents way ahead of time

Even if April 18 is still a ways off, it’s never too early to start gathering all the necessary documentation to get it done.

Here are the main tax documents and items you’ll need to file:

- All of your personal info (SSN, bank info for direct debit/deposit, etc.)

- Dependent info (their SSNs, childcare records, etc.)

- Sources of income (1099s, W-2s, unemployment records)

- Rental income (Form 1040-ES)

- Savings, investments, and dividends info (i.e., tax documents you can print from Robinhood, Coinbase, etc.)

- Health Savings Account (HSA) reimbursements

- Records of miscellaneous income (jury duty, prizes and awards, trusts, alimony, etc.)

If you’re self-employed or a freelancer, you’ve probably heard someone say “Keep your receipts.” They’re referring to all the stuff that folks with 1099s will want to keep track of for tax purposes, including:

- All 1099s and derivatives (1099-MISC, 1099-K, 1099-NEC)

- Records of all expenses (i.e., gas receipts, business flights, home office expenses, etc.)

- Records of quarterly tax payments already made (Form 1040-ES)

Now, if you’re a freelancer like me and you’re feeling nervous, don’t fret. We have a whole guide on how much you should budget for self-employed taxes as a freelancer.

Plus, we’ll discuss what tax software to use in Step 5.

Speaking as someone who’s filed both W-2 and 1099 taxes in my professional career, I can say that the latter is more tedious, but it’s not that hard.

5. Consider whether you’ll DIY or hire a pro

Now that you’ve gathered all your documents, what’s next? Should you give it a shot yourself? Or hire a tax professional from the start?

Well, let’s survey your options first and then pick which is right for you.

What are my options?

You generally have three main options for filing your taxes:

- Use IRS Free File — If you made less than $73,500 in 2022, you might qualify to file your taxes for free through the IRS Free File program. Basically, the IRS will link you out to one of a handful of third-party providers who aren’t supposed to charge you anything to file.

- Use a tax filing software like TurboTax — If you made above $73,500 or simply don’t mind paying for a slightly more optimized experience, you can use a tax filing program like TurboTax or TaxSlayer to file your taxes online. And since these programs are hyper-competitive, they tend to make it better and easier every year. Check out the best tax software programs.

- Hire a tax professional — Your third and final option is to hire a human tax pro to do it for you. This can cost anywhere from $300 to $1,000, which sounds pricey, but it can easily be worth it in certain scenarios. Not only does this take stress off your plate, but a good tax pro can maximize your refund and earn you more than they charge. Plus, if they’re generous with their time, they can mentor you and ask questions so you’re better equipped to DIY next year.

At this point you’re probably wondering how easy it is to DIY, so let’s discuss.

Which should I pick? Self-file or hire a pro?

In general, salaried employees have it way easier than self-employed folks.

If you’re a W-2 employee with no dependents, filing your taxes is going to be a breeze. You can DIY online in well under an hour, and with practice, you can knock it out each year in under 10 minutes.

However, if you’re a hustler/freelancer like me with multiple 1099s, tons of business expenses throughout the year, and a drawer bursting with receipts, it might make sense to call for backup. As mentioned, tax pros aren’t cheap, but they can save you more than they charge.

The CPA I hired not only taught me how to file my self-employment taxes correctly, but he recommended a restructuring of my business that would save me tens of thousands in the long run (thanks, Chad).

Read more: Should I hire a tax preparer?

6. Pay your taxes (or get your refund later)

Once you file your taxes, you’ll either owe the IRS a big chunk of money — or you’ll get a chunk of money in return.

So, which will it be, and how do you pay/receive it?

How to know if you’ll be paying taxes or getting a refund

Generally speaking, most W-2 employees will be getting a tax refund. That’s because your employer withholds federal taxes from your paycheck, and the IRS is refunding the amount you’ve already overpaid.

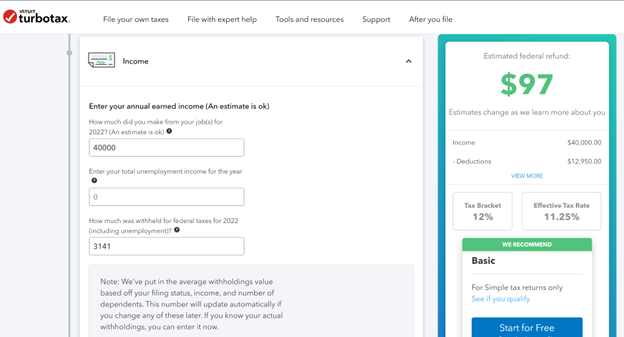

If you have your W-2 in front of you, you can plug some numbers into TurboTax’s free tax calculator to see your rough return before other factors (dependents, credits, etc.).

Source: TurboTax

If you’re self-employed/1099 and have been making quarterly tax payments throughout the year, you may also be entitled to a refund. For more on how quarterly payments work, check out Rules 3 and 4 of 5 valuable tips for the self-employed.

Lastly, self-employed/1099 folks who have not made quarterly tax payments yet will owe the IRS the whole year’s taxes by April 18. This is typically a big number (depending on how much you earned) plus a small fee for not making quarterly payments, so be sure to estimate it today and get ready!

(Personally, I like to keep my future tax payments in a high-yield savings account so it’s accessible, but still earns interest before I hand it to the IRS).

Read more: Best high-yield savings accounts

How to pay the IRS for the money you owe

If you owe money, your filing software will help you submit an electronic payment to the IRS.

Now, the IRS will take credit cards, but you still shouldn’t pay this way for a few reasons:

- There’s usually a ~2% fee which wipes out any potential rewards points.

- Even if your tax payment triggers a sign-up bonus (e.g., spend $4,000 to earn $500), your bank may disqualify it as a non-qualifying purchase.

- Putting your tax payment on your credit card could hurt your credit score by increasing your utilization ratio and the chances that you’ll miss a payment. And if you do miss a payment, the interest rate could be sky-high and send you into spiraling debt.

So… yeah. Please don’t pay your taxes with a credit card. It’s always best to direct debit your checking or savings account instead.

How to receive your tax refund

On the flip side, if Uncle Sam owes you money, you can either request a check or a direct deposit.

Request the direct deposit. You’ll get it way faster, there’s no chance of losing it, and it saves a small sliver of a tree.

According to the IRS, you should receive your refund within 21 days of your e-filing being accepted. You can always track your money via the IRS’s Where’s My Refund? tool.

Tax term glossary

Now that we’ve run through the ins and outs of filing your taxes, here are some terms you’ll probably come across, and what they each mean:

- Adjusted Gross Income, or AGI – This is your total income from all sources, like contributions to retirement plans, alimony paid, or certain deductions for the self-employed.

- Alternative Minimum Tax, or AMT – This is a special tax designed to prevent high-income taxpayers from using so many tax breaks that their actual tax liability is reduced to zero or very close to it.

- Audit – When the IRS requests that you document that you have correctly reported your income and deductions. Most are done by mail and involve specific questions the IRS has.

- Capital gains and losses – When you sell an asset for more or less than it’s worth, the gain or loss is referred to as a capital gain or loss. Generally speaking, a gain is taxable, and a loss is deductible.

- Credits – Allowances by the IRS for specific dollar amounts that directly reduce your income tax liability.

- Deductions – Certain expenses you incur can be deducted from your income for tax purposes. Examples include payment of mortgage interest and contributions to retirement plans.

- Dependent – This is someone who relies on you to provide for their support. There is no longer a deduction for dependents, but having one or more can be important in certain tax calculations.

- Exemptions – Prior to 2018, you could take a deduction for yourself, your spouse, and any dependents you had. The deductions represented a reduction in taxable income. They no longer apply through 2023.

- Estimated tax payments – The U.S. tax code is based on a pay-as-you-go process. That is, you pay tax on income as you earn it. Income that is not subject to withholding, such as by an employer, requires payment of quarterly estimated tax payments.

- Gross income – This is your taxable income from all sources, prior to adjustments and deductions. It typically includes wages, interest, capital gains, retirement income, and other sources.

- Head of household – This is the filing status for a person who is unmarried but who pays more than half the cost of maintaining a home for themselves and a qualifying person, usually a dependent.

- Itemized deductions – The IRS permits the deduction of certain expenses from your taxable income. Those include medical expenses, state and local taxes paid, mortgage interest, and charitable deductions. However, to take these deductions, they must collectively exceed your standard deduction.

- Marginal tax rate – This is the highest rate at which your income is taxed, based on your highest tax bracket.

- Standard deduction – This is a flat dollar amount you’re allowed to deduct from your taxable income, instead of itemizing your deductions. It benefits those who don’t have sufficient deductions to itemize.

- Tax bracket – Tax brackets are the percentages in that chart at the top of this article. That’s why the phrase “She’s in a higher tax bracket” is nerdy slang for “She’s making good money.”

- Tax write-offs – Tax write-offs, aka deductions, are legitimate business expenses that you can subtract from your taxable income. For example, if your business makes $500,000 and spends $50,000 on a work truck, you can “write off” the truck and only be taxed for $450,000 worth of income.

- Withholding – This is the amount of estimated tax withheld by your employer, based on the income you earn. It will represent a credit toward the taxes you owe when you file your return.

Summary

That’s about it! Taxes 101. And aside from higher tax brackets each year and the occasional new tax bracket, most of this fundamental stuff doesn’t change year-over-year. Which means now you know it for life.

Featured image: create jobs 51/Shutterstock.com

Read more:

About the author