Betterment and Wealthfront are the two largest independent robo-advisors in the field, and probably the best-known. The two platforms are on the leading edge of online, automated investing, and both have been steadily expanding their menu of investment options. In fact, Wealthfront recently released a feature to automatically invest excess cash from your checking or cash account in a taxable investment account, cash account, Roth IRA, traditional IRA, or 529 College Savings Account.

It’s probably not an exaggeration to say that most investors begin their robo-advisor search with one or both these platforms.

Betterment vs. Wealthfront – which is the better of the two? Let’s drill down into the details and see if we can come to a conclusion.

What’s Ahead:

Betterment vs. Wealthfront summary

We’re going to get into considerable detail in analyzing the differences between the two robo-advisors. But the table below summarizes and compares the basic service levels and other features offered by each investment platform:

Features Betterment Wealthfront

Minimum Initial Investment $10 to get started $500

Accounts Available Individual and joint taxable accounts; traditional, Roth, SEP and rollover IRAs; trusts and non-profits Individual and joint taxable accounts; traditional, Roth, SEP and rollover IRAs; trusts and 529 plans; crypto trusts

Advisory Fees Digital: 0.25% to $2 million; 0.15% over $2 million; Premium: 0.40% to $2 million; 0.30% over $2 million 0.25%

Tax-loss Harvesting Yes Yes

Rebalancing Yes Yes

Dividend Re-investing Yes Yes

Mobile App Android & iOS devices Android & iOS devices

Socially Responsible Investing Yes Yes, through Smart Beta and Stock-level Tax-loss Harvesting (min. Investment $100,000)

Smart Beta Yes Yes with $500,000 minimum investment

Betterment is not a licensed tax advisor. Tax Loss Harvesting+ is not suitable for all investors. Investing involves risk. Performance not guaranteed.

About Betterment

![]()

Betterment is the largest independent robo-advisor in the industry, with at least $33 billion in assets under management. The company was founded in 2008, and is based in New York City.

Like all robo-advisors, Betterment uses Modern Portfolio Theory (MTP) to create and manage your investment portfolio. MPT stresses proper asset allocation based on targeted risk levels.

Signing up for Betterment

You can sign up for the platform with no money at all. The first step will involve completing a brief questionnaire, that will identify your investment goals, time horizon, and risk tolerance level.

Your portfolio will then be created from a mix of 12 different asset classes, including six for stocks and six for fixed-income investments. Each asset class will be represented by an individual exchange traded fund (ETF), giving your portfolio exposure to literally thousands of individual securities. Each ETF is tied to an index representing the entire asset class it represents.

Once your portfolio has been created, it will be fully managed on an ongoing basis. That will include automatic dividend reinvesting, periodic rebalancing to maintain target asset allocations, and even tax-loss harvesting to minimize capital gains taxes in taxable accounts.

The use of index-based ETFs and automated investment management keeps investing expenses low, maximizing your investment returns. Betterment offers both taxable and tax-sheltered retirement accounts.

Learn more about Betterment: read our full review or visit their site.

About Wealthfront

Wealthfront is the second largest independent robo-advisor, with at least $10 billion in assets under management. The company is based in Redwood City, California, and began operations in October, 2011.

Wealthfront works much the same as Betterment and other robo-advisors. It uses modern portfolio theory, and invests your money in various asset classes, each represented by an index-based ETF. However, Wealthfront allocates your portfolio across fewer – but more diversified – asset classes.

For example, it uses just three stock classes – US stocks, foreign developed stocks, and emerging market stocks. It also uses just four fixed income classes, one of which is dividend stocks, which may add a growth component to an income generating asset class.

But where Wealthfront departs from Betterment is that it also diversifies into natural resource stocks and real estate investment trusts. The two asset classes give you a broader investment mix, as well as provide a large measure of protection against inflation. Oh, and you can even invest in crypto now! Wealthfornt offers two crypto trust options: Grayscale Bitcoin Trust (GBTC) and Grayscale Ethereum Trust (ETHE).

Wealthfront’s time-saving technology can help you invest more, too. Their latest feature addition allows you to have the robo-advisor monitor a checking or cash account for excess funds. When your account exceeds the cash limit you set, they automatically invest the excess into a qualifying account type of your choosing, including IRAs and 529 College Savings Accounts. This technology is smart enough to watch out for recurring transfers, as well, so it doesn’t accidentally mess up your future financial plans.

Signing up for Wealthfront

Like other robo-advisors, Wealthfront starts by having you complete a questionnaire, the answers of which will provide the basis of your portfolio.

You need a minimum of $500 to begin, then Wealthfront fully manages your portfolio, including automatic dividend reinvesting, periodic portfolio rebalancing, and tax-loss harvesting.

Once again, the use of automated investing and index-based ETFs enables Wealthfront to provide professional portfolio management at a very low fee.

Learn more about Wealthfront: Read our full review or visit their site.

Betterment vs. Wealthfront: Investment performance

We thought it would be helpful to include a comparison of investment performance between the two robo-advisor giants. However, due to limited performance data provided by Betterment, the comparison is no better than approximate. Also, individual portfolios will vary in their asset allocations based on investment goals, time horizons, and investor risk tolerance.

In the absence of an exact side-by-side comparison of precisely matching portfolios, we’ve done some number crunching and come up with what we believe to be a reasonable approximation of the investment performance for both over the past few years.

Betterment

Note: Betterment’s historical performance tool has been deprecated. The information below was collected by Money Under 30’s editorial team via the tool in 2019.

Betterment once provided a historical performance tool that offered somewhat limited investment return data. The screenshot below shows an interactive graph enabling you to calculate returns over various time frames, going all the way back to 2004 (which is a tad meaningless, given the platform was only launched in 2008).

We set the graph from October 2011, because it lines up with Wealthfront’s data going back to its inception on October 14, 2011. However, the Betterment results only extend through July 2018, while Wealthfront’s are continuous, allowing us to use results through February 2019.

Betterment’s investment results from October 2011, through July 2018, show an 82.6% return, based on a portfolio with an 80% stock allocation.

But in doing our best to maintain a relative apples-to-apples comparison, we blended the performance of the 80% stock allocation with a 70% allocation, because that aligns more consistently with Wealthfront’s stock allocations. That produces a blended return of 77.8% over 82 months. That works out to an average annual return of just under 8.8%.

Wealthfront

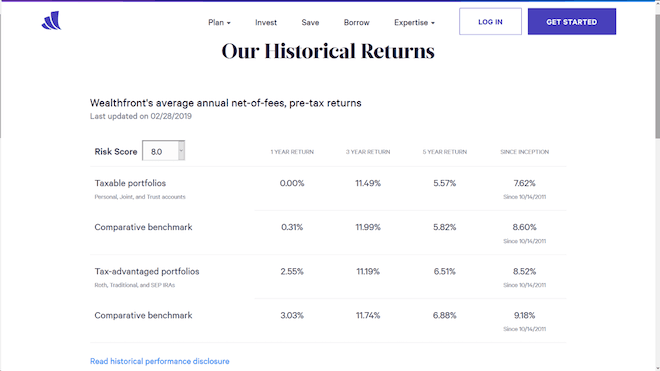

Wealthfront provides a regularly updated report on its historical returns. The screenshot below shows Wealthfront investment results through February 28, 2019, for both taxable portfolios and tax-advantaged portfolios (retirement accounts).

They’re displayed for one year, three years, five years, and since the inception of Wealthfront on October 14, 2011.

Now as is always the case with investment returns, these results require a significant amount of explanation. The investment return for each time frame is compared with a comparative benchmark. The benchmark includes the same asset allocations and ETFs used in the actual portfolios with the same risk scores.

However, the benchmark does not include advisory fees or trading costs due to bid/ask spreads. As a result, the Wealthfront investment results are consistently slightly below the corresponding comparative benchmark.

Both the taxable and nontaxable portfolios are weighted heavily in favor of US and international stocks. The taxable portfolio includes upwards of 80% in stocks, with the balance invested in fixed income, natural resources, and real estate. Nontaxable portfolios have a somewhat lower stock allocation, again with the balance invested in fixed income, natural resources, and real estate.

The above results are for a portfolio based on an investor with a risk score of 8.0. This is just one of 20 potential asset allocations, since the Wealthfront risk scores run in increments of .5, from .5 up to 10. The results will be different for each risk score level, which is part of what makes it difficult to make a direct comparison with Betterment or any other investment platform.

Betterment vs. Wealthfront Investment performance conclusion

Based on the numbers above, Betterment has an average annual investment return of just under 8.8%. Wealthfront is at 7.62% on its taxable portfolios, and 8.52% on its tax-advantaged portfolios.

While it may appear that Betterment has the better performance, be reminded that there are timing differences. Notably, the data on Betterment runs only through July, 2018.

Given that the fourth quarter of 2018 was unusually volatile, that can skew the performance data in favor of Betterment. As well, Wealthfront discloses that their performance numbers account for advisory fees and bid/ask spreads, while Betterment is silent on this issue.

So there you have it – it’s not quite an apples-to-apples comparison, but it’s as close as we can get based on the public data available.

Betterment and Wealthfront pros

Betterment:

- $10 to get started

- Human assisted investment advice.

- Tax-loss harvesting on all taxable accounts.

- Customer support includes live chat.

- One low fee of 0.25% on all accounts up to $2 million.

- Fee drops to 0.15% on accounts above $2 million.

- Stock allocations include large- , medium- , and small-cap value stocks.

- Smart Beta option.

- Socially responsible investment option.

- Unlimited access to a team of financial advisors with an annual fee of 0.40% (minimum $100,000 balance).

- External account analysis, including 401(k) plans.

Wealthfront:

- Low minimum initial investment, at $500.

- Low annual advisory fee of 0.25% on all account balances

- Your portfolio includes natural resources stocks and real estate.

- Crypto investment trust options.

- Financial planning tools.

- Portfolio line of credit available on account balances over $100,000.

- Cash account option.

- Smart Beta option.

- Socially responsible investment option.

- 529 college savings accounts available.

- Individual stocks used in larger portfolios.

- Automatically invest excess cash into qualifying accounts, including IRAs and 529 College Savings Accounts.

Betterment and Wealthfront cons

Betterment:

- No diversification into alternative investments, like real estate and natural resources.

- Provides analysis of external accounts, but does not consider them in asset allocations.

Wealthfront:

- No reduction in fees for larger portfolios.

- $500 required to open an account, though this is not a major obstacle.

- Smart Beta option requires minimum investment of $500,000.

Why choose Betterment?

Use of value stocks

Betterment’s asset allocation includes small-, medium-, and large-cap value stocks in each portfolio. This holds the potential to outperform the general stock market, as measured by the S&P 500.

Value stocks represent companies that are largely shunned by investors, but are fundamentally sound, and can produce above average gains over the long term.

Financial advisors available on portfolios over $100,000

Betterment’s Premium plan offers access to live financial advisors, and an annual advisory fee of just 0.40%. This is a fraction of the 1% to 2% fee charged by traditional human financial advisors.

Betterment also offers a series of financial advice packages, with fees ranging from $299 to $399. The packages address basic financial planning, such as preparing for college, marriage, and retirement.

Socially Responsible Investing (SRI)

Betterment replaces emerging market stocks and large-cap US stocks with three ETFs dedicated to socially responsible investing. Your entire portfolio won’t be fully SRI, but a large portion will be.

Smart Beta

Managed by Goldman Sachs, this portfolio offers investments with the potential to outperform the conventional market cap strategy. It involves an actively managed portfolio, offering potentially higher rewards with correspondingly higher risks. This portfolio requires a minimum investment of $10.0.

Betterment Cash Reserve

Betterment Cash Reserve offers a 2.25% APY. You won’t need a minimum balance and you’ll pay no monthly fees. Plus, you’ll also be able to make an unlimited number of withdrawals (typically, you can only make six).

For Cash Reserve (“CR”), Betterment LLC only receives compensation from our program banks; Betterment LLC and Betterment Securities do not charge fees on your CR balance.

Betterment Checking

Betterment also offers a checking account that comes with no fees, mobile check deposit, no minimum balance, and reimbursed ATM fees. But the best part of this checking account is that, thanks to Betterment’s partnership with Dosh, you’ll also get the Betterment Visa® Debit Card that offers cash back when you use your card at participating businesses. These include more than 10,000 merchants across the globe, covering both online and in-person payments. You can easily locate participating merchants in Betterment’s mobile app. If you want to shop online, note that you do need to shop through Betterment’s “Earn Rewards” section in the app or on the site.

Your cash back offers are also tailored to your own personal buying preferences. That means you’ll see offers that apply specifically to the restaurants, shops, and other businesses that fit your own interests. Your cash back rewards are automatically deposited into your checking account in real-time, so you don’t have to wait to redeem them. You may even see multiple cash back deposits all within the same day! And you’ll be notified every time Betterment finds rewards for you, making it easy to keep track of how much you’ve earned.

Flexible Portfolios

This option allows you to adjust the individual asset class weights in your portfolio. It’s an option intended only for seasoned investors, providing some control over portfolio allocation, while still enjoying the benefits of automated investing.

Why choose Wealthfront?

Smart Beta

Similar to Betterment, Wealthfront’s Smart Beta seeks to outperform the general market. It does this by deemphasizing market capitalization as a primary factor in portfolio construction. This leads to a more even distribution of stocks within the portfolio. It represents a form of active portfolio management, and is available for portfolios of $500,000 or more.

Stock-level tax-loss harvesting

This might be Wealthfront’s most interesting feature. They offer three different portfolios that enable you to diversify into individual stocks. For example, up to 500 stocks will be purchased out of the S&P 500 index. Depending on the account size, up to 1,000 stocks will be chosen from the S&P 1500 index. These portfolios allow for greater efficiency with tax-loss harvesting, since individual stocks offer more flexibility than entire ETFs. This category requires a portfolio between $100,000 and $500,000.

Wealthfront Risk Parity

This is a more complex investment strategy, but one that has shown higher long-term returns. It does this by allocating the portfolio in a way that equalizes the risk contributions of each asset class. Since the strategy uses leverage with certain positions in the portfolio it is higher risk. Participation does require a larger account balance.

Wealthfront Portfolio line of credit

This line is available for clients with accounts totaling $100,000 or more. It enables you to borrow up to 30% of your account value, and make repayments on your own schedule.

The line of credit is secured by your portfolio, which eliminates application or qualification based on credit or income. It’s not designed to be a margin loan, but it offers you total flexibility. Funds can be borrowed for any purpose, and since you’re borrowing from yourself, you can repay on your own terms.

Wealthfront Path

This is something of a financial advisory, but it’s software-based. It provides financial planning tools to help you plan for retirement, home ownership, saving for the down payment on a house, and college funding for your children.

The app can be used to run “what if scenarios”, such as seeing the projections of increasing your savings or determining how much financial aid your child might be eligible for in college. You can even look for a house through the connection with Zillow.com.

Technology that invests excess cash

When money is managed manually, it’s possible to hesitate when it comes time to invest. Wealthfront’s latest technological addition automates the process by investing excess cash above a limit you set.

In the past, this could only be done with a taxable investment account or cash account. Today, the technology has been improved to include the option to invest in Roth IRAs, traditional IRAs, and 529 College Savings Accounts.

Final thoughts on Betterment vs. Wealthfront

Betterment and Wealthfront have become the largest independent robo-advisors because they’ve been in the forefront of the phenomenon that is automated investing. Both have a long line of satisfied investment clients, and each has continued to innovate from the basic robo-advisor model.

Which is the better of the two? There is no definitive answer to that question. It really depends on the various services and features each provides that will best fit your own personal needs.

For example, if you prefer diversification into alternative investments, like real estate and natural resources, Wealthfront will be your choice. But if you prefer investing in expert-built, curated portfolios, Betterment will be the better option.

Otherwise, the two platforms are largely identical. Considering the direct competition between the two, that’s hardly surprising. Each charges a basic fee of 0.25% for the vast majority of investors. Each offers smart beta, socially responsible investing, various forms of financial advice, and the ability to open an account with little or no money.

Summary

In the final analysis, both Betterment and Wealthfront platforms. In fact, where each has distinguished itself from the many robo-advisor platforms now available is that they have trade-up options. As your portfolio grows, each offers the ability to take advantage of more sophisticated investment options. These are the kind of investment strategies more typically available with higher cost, traditional investment advisors.

In truth, you can’t go wrong with either of these platforms. Look carefully at the features that will work best for you, and make your choice accordingly.

Betterment Cash Reserve Disclosure - Betterment Cash Reserve ("Cash Reserve") is offered by Betterment LLC. Clients of Betterment LLC participate in Cash Reserve through their brokerage account held at Betterment Securities. Neither Betterment LLC nor any of its affiliates is a bank. Through Cash Reserve, clients' funds are deposited into one or more banks ("Program Banks") where the funds earn a variable interest rate and are eligible for FDIC insurance. Cash Reserve provides Betterment clients with the opportunity to earn interest on cash intended to purchase securities through Betterment LLC and Betterment Securities. Cash Reserve should not be viewed as a long-term investment option. Funds held in your brokerage accounts are not FDIC‐insured but are protected by SIPC. Funds in transit to or from Program Banks are generally not FDIC‐insured but are protected by SIPC, except when those funds are held in a sweep account following a deposit or prior to a withdrawal, at which time funds are eligible for FDIC insurance but are not protected by SIPC. See Betterment Client Agreements for further details. Funds deposited into Cash Reserve are eligible for up to $1,000,000.00 (or $2,000,000.00 for joint accounts) of FDIC insurance once the funds reach one or more Program Banks (up to $250,000 for each insurable capacity—e.g., individual or joint—at up to four Program Banks). Even if there are more than four Program Banks, clients will not necessarily have deposits allocated in a manner that will provide FDIC insurance above $1,000,000.00 (or $2,000,000.00 for joint accounts). The FDIC calculates the insurance limits based on all accounts held in the same insurable capacity at a bank, not just cash in Cash Reserve. If clients elect to exclude one or more Program Banks from receiving deposits the amount of FDIC insurance available through Cash Reserve may be lower. Clients are responsible for monitoring their total assets at each Program Bank, including existing deposits held at Program Banks outside of Cash Reserve, to ensure FDIC insurance limits are not exceeded, which could result in some funds being uninsured. For more information on FDIC insurance please visit www.FDIC.gov. Deposits held in Program Banks are not protected by SIPC. For more information see the full terms and conditions and Betterment LLC's Form ADV Part II.Read more:

- Betterment Review: The Way Investing Should Be

- Wealthfront Review: Automated Investing And Financial Planning That’s Free Up To $10,000

About the author